Incontinence Care Supplies: What Insurance Covers (and What It Doesn't)

<article>

Will Medicare or Medicaid Cover My Incontinence Supplies?

sbb-itb-45288fe

Struggling to afford incontinence supplies? Over 50% of Medicare beneficiaries face this challenge because Original Medicare doesn’t cover absorbent products like adult diapers or pads. Medicaid programs in most states, however, do provide coverage for these items if deemed medically necessary. Here's what you need to know to navigate insurance coverage and manage costs.

Medicare classifies disposable incontinence supplies as “personal comfort” items, leaving beneficiaries to pay out-of-pocket. Medicaid, on the other hand, offers better support, with 45 states covering products like adult briefs and underpads. Some private insurance plans may reimburse costs, but coverage varies widely. To reduce expenses, explore manufacturer discounts, subscription services, or programs like PeelAways, which provide practical alternatives.

Understanding your insurance policy is key. Contact your provider to confirm benefits, and ensure you have a doctor’s prescription for medically necessary supplies. If claims are denied, appeal promptly - most Medicare appeals succeed. For uncovered items, financial assistance programs or local resources like diaper banks can help ease the burden.

</article>

What Incontinence Supplies Does Insurance Usually Cover?

Insurance Coverage for Incontinence Supplies: Medicare vs Medicaid vs Private Insurance Comparison

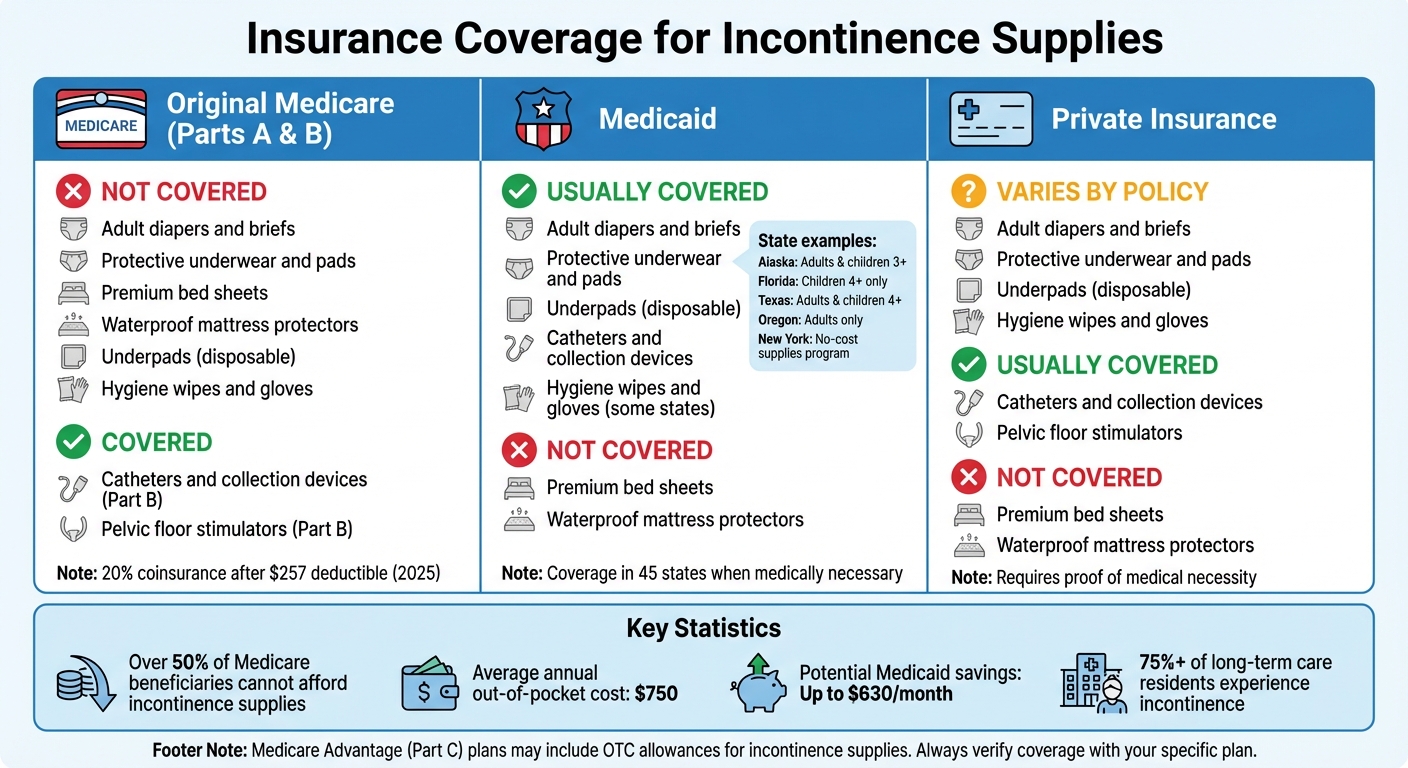

Insurance policies differ when it comes to covering incontinence supplies. Medicare Part B provides coverage for certain durable medical equipment if prescribed by a doctor, while Medicaid in many states includes disposable supplies deemed medically necessary. Below is a breakdown of how Medicare, Medicaid, and private insurance approach coverage for these items.

Medicare Coverage for Incontinence Supplies

Original Medicare (Parts A and B) does not cover disposable incontinence supplies like adult diapers, pads, or protective underwear. These items are categorized as personal comfort products, not medical necessities.

However, Medicare Part B does offer coverage for durable medical equipment prescribed by a doctor. This includes items like urinary catheters (indwelling, condom, or intermittent), external urinary collection devices, and pelvic floor stimulators. Once you meet the Part B deductible (currently $257 for 2025), you are generally responsible for 20% coinsurance for these products.

Medicare Advantage (Part C) plans must cover all Original Medicare benefits but often go further by including allowances for over-the-counter incontinence supplies. These additional benefits vary by plan and region. To confirm your specific benefits, consult your plan’s Evidence of Coverage or contact your plan provider.

Medicaid Coverage by State

Most state Medicaid programs cover disposable incontinence supplies, but the specifics differ depending on where you live. Commonly covered items include bladder control pads, adult pull-ons, adult briefs, pediatric diapers, booster pads, underpads, gloves, and wipes - provided they are deemed medically necessary with a diagnosis and a doctor’s order.

Here are some examples of state-specific coverage:

| State | Coverage Details |

|---|---|

| Alaska | Covers adults and children ages 3+ |

| Florida | Covers children ages 4+; no coverage for adults |

| Texas | Covers adults and children ages 4+ |

| Oregon | Covers adults only |

| New York | Offers no-cost supplies through the Medicaid Incontinence Supply Program |

| California | Coverage varies by plan |

For individuals who qualify for both Medicare and Medicaid (dual eligibility), Medicaid typically covers disposable supplies that Medicare does not. To learn more about your state’s program, contact your local Medicaid office for details on monthly supply limits or brand-specific requirements.

Private Insurance Coverage

Private insurance policies handle incontinence supplies differently, depending on the plan and state regulations. Some insurers reimburse for items like protective underwear, wipes, and bed pads, while others exclude absorbent products, much like Medicare. Often, coverage depends on providing proof of medical necessity from a healthcare provider.

To confirm your benefits, check the details of your insurance policy or contact the customer service number on your insurance card. In some cases, you might need to submit a Certificate or Letter of Medical Necessity from your doctor to qualify for reimbursement. Taking the time to review your policy ensures you get the most out of your coverage.

What Incontinence Supplies Are Not Covered by Insurance?

Knowing which incontinence supplies aren't covered by insurance is essential for budgeting, especially since these items can cost an average of $750 annually out-of-pocket. Unfortunately, disposable absorbent products, waterproof mattress protectors, and premium bed sheets are typically excluded from coverage. Here's why these items fall outside insurance policies.

Why Certain Items Aren't Covered

The main reason lies in how insurance defines Durable Medical Equipment (DME). To qualify as DME, an item must be reusable, prescribed by a doctor, and serve a medical purpose beyond personal hygiene. Disposable products like adult diapers and bed pads don’t meet these criteria because they’re single-use items. Even high-end versions with advanced features are still considered disposable personal care products.

This classification has a widespread impact. Over half of Medicare beneficiaries who need incontinence supplies cannot afford them, placing a heavy financial burden on families and caregivers. The issue is even more pronounced in long-term care facilities, where over 75% of residents experience incontinence.

Covered vs. Non-Covered Supplies: A Comparison

Here’s a breakdown of what’s typically covered versus excluded across different insurance types:

| Supply Type | Original Medicare | Medicaid | Private Insurance |

|---|---|---|---|

| Adult diapers and briefs | Not covered | Usually covered | Varies by policy |

| Protective underwear and pads | Not covered | Usually covered | Varies by policy |

| Premium bed sheets | Not covered | Not covered | Not covered |

| Waterproof mattress protectors | Not covered | Not covered | Not covered |

| Catheters and collection devices | Covered (Part B) | Usually covered | Usually covered |

| Pelvic floor stimulators | Covered (Part B) | Varies by state | Usually covered |

| Underpads (disposable) | Not covered | Usually covered | Varies by policy |

| Hygiene wipes and gloves | Not covered | Covered in some states | Rarely covered |

Medicaid tends to offer better coverage for disposable supplies compared to Medicare and private insurance plans. If you're eligible for both Medicare and Medicaid, your state's Medicaid program will likely cover the disposable items Medicare excludes.

How to Verify and Maximize Your Insurance Benefits

Making sure your insurance coverage aligns with your needs can save you hundreds of dollars each year, especially when managing incontinence care expenses. To start, call the customer service number on your insurance card. Ask specifically if your plan includes coverage for "Durable Medical Equipment" (DME) or offers an "Over-the-Counter benefit" for incontinence products. Be prepared with your Member ID, plan name, and the primary insured person’s details when making the call.

How to Review Your Insurance Policy

Insurance companies classify incontinence supplies differently, which can impact your out-of-pocket expenses. Items like catheters and pelvic floor stimulators are often categorized as Durable Medical Equipment (DME), while products like adult diapers are considered personal hygiene items. For example, Original Medicare Part B covers 80% of DME costs after you meet the annual deductible, leaving you responsible for the remaining 20% as coinsurance. However, according to Medicare.gov, "Medicare doesn't cover incontinence supplies or adult diapers".

Check your Evidence of Coverage document for an OTC allowance. This benefit provides a monthly credit that can be used to purchase incontinence products. Medicaid coverage, on the other hand, varies by state. In 45 states and Washington, D.C., absorbent supplies are covered when deemed medically necessary, potentially saving you as much as $630 per month.

Once you understand your policy details, you’ll be better equipped to file claims successfully.

How to Submit Claims Successfully

Most insurance providers require proof that incontinence supplies are medically necessary. To meet this requirement, have your doctor document your diagnosis and issue a signed Certificate of Medical Necessity. Nexwear explains: "Your health-care provider must have deemed incontinence products medically necessary, and you must have a current diagnosis for loss of bladder or bowel control".

Using a Medicare- or Medicaid-accredited supplier can simplify the claims process. These suppliers handle coverage verification, coordinate with your doctor for prescriptions, and manage the necessary paperwork, including monthly refills. Common reasons for claim denials include using out-of-network suppliers, failing to meet age requirements (some Medicaid plans require patients to be at least 3 years old), or lacking a qualifying medical diagnosis.

If your claim is denied, don’t stop there - move on to the appeals process.

How to Appeal Denied Claims

When a claim is denied, it’s important to act quickly. Medicare patients who appeal denials win about 80% of the time, yet only 11% actually file appeals. You typically have 180 days from the date of the denial notice to file an internal appeal with your insurer.

The key to a strong appeal is a Letter of Medical Necessity from your doctor. This letter should outline your diagnosis and explain why the denied supplies are essential. To ensure your appeal is received, send all documents via certified mail with a return receipt requested. Also, keep detailed records of the date, time, representative names, and key points from your conversations with the insurance company.

Medicare appeals involve a five-step process: Redetermination, Reconsideration by an Independent Contractor, Administrative Law Judge Hearing, Appeals Council Review, and Federal District Court. About 50% of first-level appeals result in overturned denials. As Jen Teague, Director for Health Coverage and Benefits at NCOA, advises: "Appealing Medicare coverage denials requires lots of patience and persistence. But since the majority of coverage denials are overturned at some point during the appeals process, it's a smart idea to just keep moving forward". If your health is at serious risk due to delays, you can request an expedited review, which typically results in a decision within 72 hours.

Affordable Options for Supplies Not Covered by Insurance

Finding ways to manage the cost of incontinence supplies not covered by insurance can make a big difference. Thankfully, there are several strategies to help reduce expenses. From bulk discounts to community programs and tax-advantaged accounts like Health Savings Accounts (HSA) or Flexible Spending Accounts (FSA), there are options to ease the financial burden.

Manufacturer Discounts and Subscription Programs

Many manufacturers and retailers offer discounts that can significantly cut costs. Signing up for manufacturer newsletters often gives access to coupons and promo codes, such as "HELLO20", which provides 20% off and free shipping on orders over $25. Subscription services can offer even better savings, with bulk order discounts ranging from 30% to 50% compared to individual purchases.

Using an HSA or FSA can also stretch your budget, as many incontinence supplies qualify for reimbursement if they’re medically necessary. To ensure eligibility, ask your doctor for a Letter of Medical Necessity. Among the various options available, PeelAways stands out as a practical and time-saving solution.

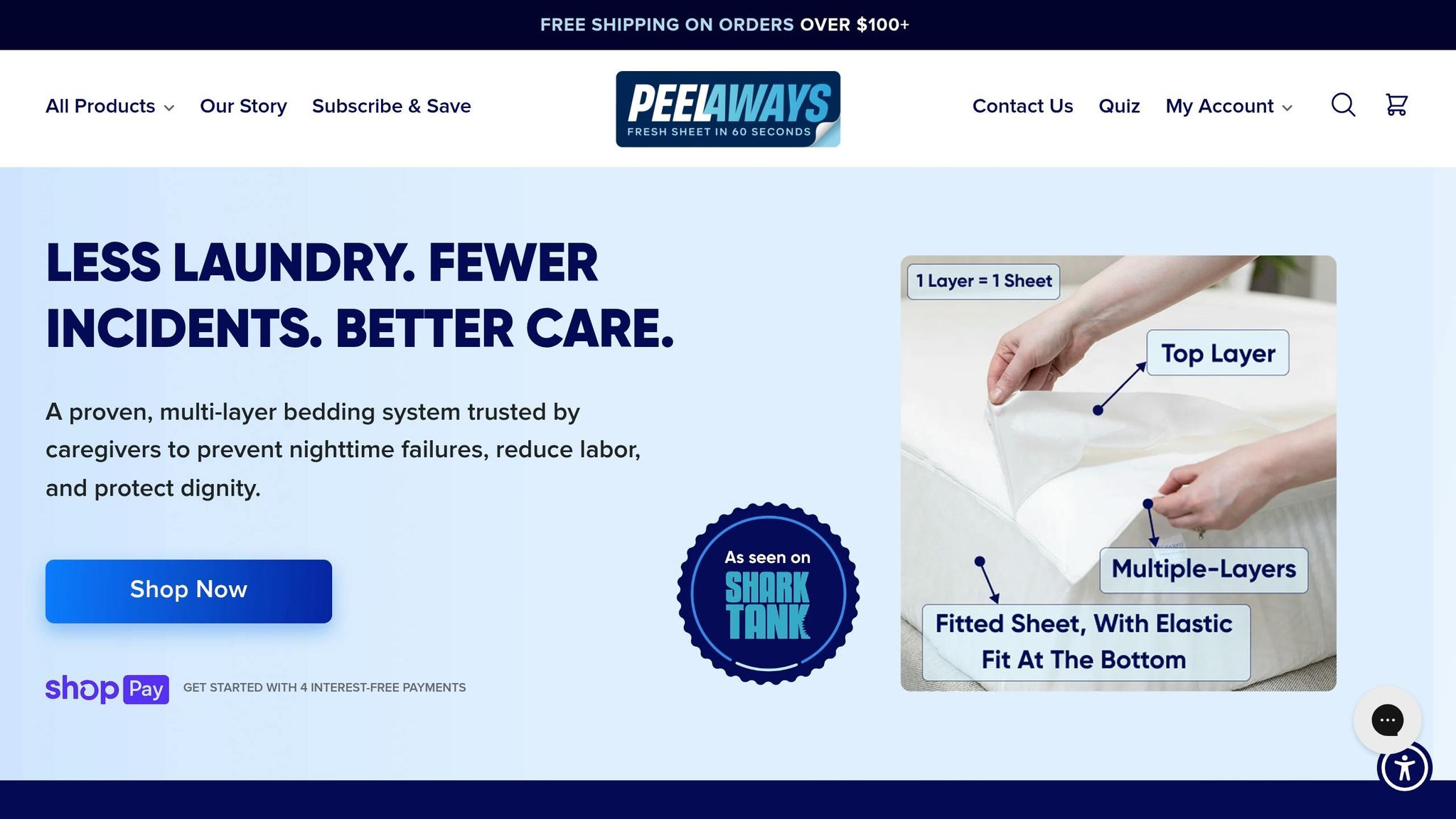

PeelAways: Multi-Layer Disposable Waterproof Bed Sheets

PeelAways sheets offer a clever solution for incontinence care. Each sheet has 5–7 waterproof layers, so when one layer is soiled, you simply peel it away to reveal a fresh, clean layer underneath - all in under a minute. This design can reduce laundry loads by up to 90% and eliminate the physical effort of lifting mattresses.

Caregiver Jalene Stanger, who looks after two incontinent teenagers, shared her experience:

"These have saved my sanity! With 2 incontinent special needs teenagers... these have relieved a lot of stress. They hold a LOT of liquid and are easy to use and tear away. No more 15 loads of laundry and wet mattresses!"

PeelAways has earned a 4.8-star rating from over 12,000 customers, making it a trusted choice for families and healthcare facilities alike. While Medicare doesn’t typically cover disposable supplies, these sheets may qualify for reimbursement through HSA or FSA accounts. Plus, you can save even more with a 15% subscription discount and free shipping on orders over $100.

Financial Assistance Programs and Resources

For those struggling with the cost of supplies, there are additional resources to explore. Medicaid programs in most states cover absorbent incontinence products when deemed medically necessary. Some Medicare Advantage (Part C) plans also include supplemental benefits, like a monthly allowance for over-the-counter items such as adult briefs and pads.

Local diaper banks are another valuable resource, often providing adult incontinence products at little to no cost. To find support, reach out to your local Area Agency on Aging or senior center. They can connect you with charitable organizations and state-specific programs that offer free or low-cost supplies.

Conclusion

Understanding insurance coverage for incontinence supplies can make managing care much easier. While Original Medicare does not cover absorbent products, Medicare Advantage plans might include them as supplemental benefits. Medicaid, on the other hand, often covers these supplies if they are considered medically necessary. The most important step is to review your specific plan details and ensure you have a prescription when required.

For items not covered by insurance, PeelAways offers a practical and cost-effective alternative. These innovative sheets feature 5–7 waterproof layers that can be peeled away in under 60 seconds, cutting laundry needs by 50–80% and reducing the physical effort of changing traditional bedding. Plus, they are eligible for HSA or FSA reimbursement, providing an affordable way to maintain dignity and manage the emotional impact of caregiving and ease the workload for caregivers. Explore how PeelAways can simplify incontinence care - available on Amazon or directly through the PeelAways website.

"To make care more affordable, PeelAways is offering blog readers an exclusive 10% discount. Use code BLOGS10 at checkout to save on PeelAways multi-layer disposable sheets. This discount can be combined with subscriptions and bundle offers, helping you maximize savings while simplifying care.

You Can Buy Peelaways On Amazon Here.

FAQs

How do I find out if my plan covers incontinence supplies?

To find out if your insurance covers incontinence supplies, start by contacting your insurance provider and carefully reviewing your policy details. It’s also a good idea to discuss your specific needs with both your healthcare provider and your insurer to clarify what’s included. Keep in mind that traditional Medicare typically doesn’t cover items like pads or pull-ups, but some Medicare Advantage plans may offer coverage. Always check directly with your plan to get the most accurate and up-to-date information.

What paperwork do I need to get supplies covered or reimbursed?

To get incontinence supplies covered or reimbursed, you’ll usually need a prescription from your healthcare provider. Medicare might cover certain supplies under Part B if they’re classified as durable medical equipment (DME) and prescribed by a doctor. Other insurers, such as Blue Cross Blue Shield, may ask for extra forms or documentation. Be sure to review your insurance provider’s specific rules to make sure your claim is processed correctly.

What should I do if my incontinence supply claim is denied?

If your claim gets denied, the first step is to carefully review the reason for the denial. Then, work with your healthcare provider and insurance company to discuss your medical needs, confirm what’s covered, and gather the necessary documentation.

When filing an appeal, include supporting medical records and, if applicable, a letter from your provider explaining why the treatment is necessary. Be sure to review your plan details closely - this is especially important for Medicare Advantage plans, as they may have specific options for coverage or appeals that differ from other plans.

Related Blog Posts

Comments

0

SAVE MONEY & WATER

Professionals & Institutions save a fortune on labor/laundry.

SUPERIOR COMFORT

The first thing our customers notice is how soft our sheets are.

100% WATERPROOF

Each layer is 100% Waterproof, perfect for spills and accidents

SAVE TIME

Change the sheet in under 1 minute without stripping the bed.

Leave a comment